Professor Peter Spencer, Dr Paulo Santos Monteiro and Professor Peter Smith discuss the Chancellor’s new Superdeduction tax allowance in the light of the findings of their recent discussion paper on corporate tax reform.

It is beginning to look as if the government is serious about changing the economic geography of this country. Indeed, with an economic campus in Darlington, an infrastructure bank in Leeds and a Freeport in Hull, this budget brings major benefits to the North East.

However, in our view the most encouraging aspect of this budget was the chancellor’s so-called Superdeduction. This gives firms tax relief for business investment along the lines of a proposal that we made in a recent discussion paper, which we argued would bring major benefits not just for the economic geography of the country but also for productivity.

The role of investment in explaining productivity growth has long been recognised, but the new growth literature suggests that it has been seriously underestimated. That is because conventional analysis focuses on the benefit of investment to the individual firm and neglects the benefits for the wider economy and in particular the gains from knowledge spillovers. These spillovers largely stem from the complementarities between innovation and investment and the way that new ideas and practices spread from organisations that invest and innovate to others.

This synergy means that supporting capital investment can have the same effect on long-run growth as subsidizing R&D. However, because capital is easier to monitor than the production of intangible knowledge, supporting investment is less vulnerable to agency problems and gaming. Although the fiscal system recognises the importance of innovation for economic growth by supporting R&D, this is an argument for subsidising investment as well as research. Moreover, support for investment would help ensure that UK innovations generate factories and jobs here rather than overseas. What is the point of encouraging home-grown companies like Dyson to build research campuses in the UK when they manufacture their innovative new products in the Far East?

The argument is set in out in our discussion paper: ‘How to better align the UK’s corporate tax structure with national objectives’.

The chancellor is allowing firms to deduct 130% of their capital expenditure from their taxable income in the two upcoming tax years; 2021-22 and 2022-23. This is unprecedented because firms have only ever been able to claim 100% and since 1984, they have only been able to deduct the cost of depreciation, making it much longer to recoup the cost.

However, the Superdeduction is not as attractive as it looks at first sight. First and foremost, it is only meant last for two years. As the Office for Budget Responsibility (OBR), point out, it will have no long run effect on the cost or stock of capital. The chancellor argued that it would nevertheless bring investment forward and help the economic recovery from the pandemic. However, he intends to raise the corporation tax rate from its current 19% to 25% in April 2023. This would have encouraged companies to delay investment until then in order to set the cost against the higher tax rate. To be cynical, it may just be that the Superdeduction is just a short-term wheeze designed to offset that stalling effect.

Moreover, although the 130% rate is unprecedented, the scale of the subsidy is certainly not unprecedented. 130% of a 19% tax rate means that taxpayers are effectively paying for 25% of the cost of investment, whereas in the past corporation tax rates of 40%, 50% and in the 1960s 60%, they were providing a much more generous subsidy, especially with 100% first-year allowances or accelerated depreciation schedules usually in place.

Nigel Lawson’s 1984 budget swept away this subsidy. It scaled back the allowances and slashed the mainstream corporation tax rate to hopefully promote enterprise, spur investment more widely and make the UK competitive internationally. Subsequent chancellors, Labour and Conservative alike, followed this policy. However, judged in terms of its effects on business investment, this policy has clearly failed.

Source: ONS Quarterly Economic Accounts

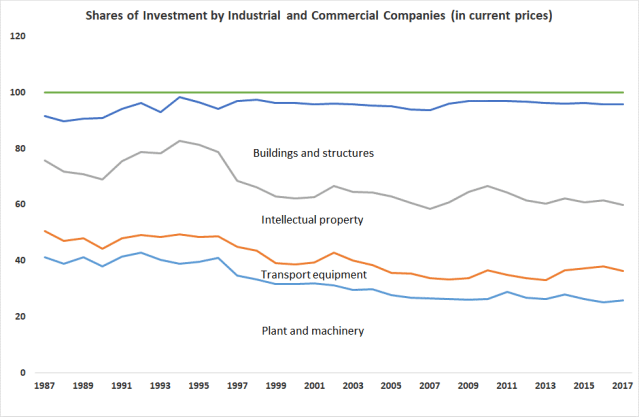

These policies have also led to a deterioration in the structure of investment. For example, in his 1997 Budget, Gordon Brown removed the ACT system that had until then provided investors with relief against double taxation of dividends (i.e. both at the level of the firm as profits and the level of the investor as dividend income). This reform was designed to encourage investment through retained profits. However, it left in place the relief on debt interest payments, which remained fully deductible from taxable profit. This anomaly favours debt at the expense of equity finance, encouraging excessive leverage, risk taking and the risk of default. It favours assets like commercial property that are easy to collateralize. Thus, it is not surprising to find that, within the declining share of investment relative to GDP, the share of buildings investment has increased markedly since 1997, while the share of investment in intellectual property and plant & machinery has declined

Source: ONS Blue Book

This brings us to the other big problem with the Superdeduction – it is poorly targeted. The need to offset the investment- delaying effect of the new 25% tax rate in 2023 meant that this subsidy had to apply to all business investment. The deadweight loss of subsidising all of the investment that would have taken place anyway means that the Chancellor is not getting very much bang for his buck. The OBR estimates that investment will as a consequence be just 10% higher by the second year 2022-23, but at the hefty cost of £12 ½ billion in both 2021-22 and 2022-23.

Having said that, we believe that the short-term investment and productivity gains from the Superdeduction will be significantly greater than the OBR has forecast. There is a lot of catching up to do and the Superdeduction will speed this up. Uncertainty over Brexit has held back investment. This uncertainty has now been resolved, after a fashion, and there needs to be a lot of investment to help restructure our industries. It is not just a matter of investing in new products and factories to exploit overseas markets but also investing to hold onto our existing European markets. There is a lot of consequent supply chain adjustment taking place already and there will have to be massive investments in battery production plants for the car industry and the like to avoid falling foul of the third country and other trade rules.

The low cost of labour has also held back investment. Immigration and late retirement have swollen the labour force and made it much cheaper to hire new staff than that to invest in new equipment labour saving equipment. In the wake of Brexit and the pandemic, many European workers have gone home and employers will find them difficult to replace, spurring investment in labour-saving machinery.

It is also encouraging to see the bias towards a lower corporation tax at the expense of allowances rate halted at last. Optimistically, it is just possible that the Treasury will come to realise the many benefits of investment and suggest that the chancellor adopts a policy that is longer-term policy and more carefully targeted. If the chancellor is serious about changing the economic geography of this country, he will be inclined to listen.