Second Year Student, Noah Kirby, discusses what the future may hold for Argentina. Originally written on December 8th 2023

Argentina’s President-Elect Javier Milei, will take control of the country on December 10th after defeating Sergio Massa’s Peronists to mark the start of a new era for Argentina under their first libertarian President. The radical self-proclaimed anarcho-capitalist has bold ambitions ‘to take a chainsaw to the state’, abolish the Central Bank and dollarise the economy in an attempt to revive and transform the Argentine economy from it’s present gloom to a competitive economic force as it was at the turn of the 20th century, but how realistic many of his policy ambitions are is still to be seen.

Milei is a very controversial figure on the Argentine political front. A former TV Economist with radical ideas for Argentina’s mounting problems, he quickly gained traction using his iconoclastic, unapologetic personality smashing central bank shaped Piñatas, posing with chainsaws and use of demeaning language regarding world leaders such as the Pope and President Lula Da Silva of close trading partner Brazil.

Despite Milei’s radical proposals initially seeming to make him an unlikely candidate, his two year old La Libertad Avanza party filled a recently opened void in Argentine politics and won the second round of elections by 11 points. The dominant political ideology in Argentina for most of modern history has been the left-wing Peronists who have overseen a high inflation, boom-bust economy for most of living memory continuously made worse by excessive spending from countless governments. The largest non-Peronist party, Juntos Por El Cambio, elected in 2015 have also been discredited for their failure to meet the targets from the IMF on their enormous $43 billion loan, missing payments while overseeing inflation rises to record levels. The impacts of continuous inflation, devaluations, and the pandemic have continued to take a toll on regular Argentines raising the poverty rate from 30% to 40% since 2015. According to a poll in March from El Universidad de San Andrés, 92% of Argentines were totally dissatisfied with the current handling of the economy. In this context, Milei offered an alternative choice under a grand vision and appealed to the Argentine electorate with change they had not seen before in the form of a hard-right economic approach to correct the tattered economy.

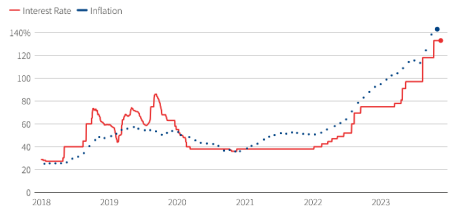

The news of Milei’s victory in the Presidential election was positively received by markets with the local Merval stock index rising by 28% and the prices of sovereign bonds maturing in 2030 (some of the most liquid bonds in Argentina) rising by 22%. Markets keenly responded to promises to modernise the Argentine economy under the guidance of Milei’s chosen Economy minister Luis Caputo, a well-respected former financier with close ties to Wall Street and the financial elite of Argentina. In a recent interview with the Financial Times, one trader in Buenos Aires described that “for the market, this is like your best friend becoming the Economy Minister”. Caputo brings more experience than Milei, being described by some as the “Messi of Finance” known for increasing access to credit for the country. As Finance Secretary under President Mauricio Macri, he restored Argentina’s access to international capital markets. Caputo’s top priority when taking office will be in the form of short-term liabilities worth 10% of GDP issued to local creditors in an attempt to reduce the money supply and control inflation. At present, this debt is being serviced by money printing continuing to fuel the 143% inflation rate in the country that is estimated by JPMorgan to rise to 210% and beyond going into next year. Caputo intends to resolve this with a direct exchange for treasury debt putting further pressure on Argentina’s weak public finances. However, this would mark a clear turning point for markets that Milei would no longer service this debt by further pushing inflation through seigniorage. Caputo will also have to renegotiate the terms of Argentina’s deal with the IMF to avoid default, all amounting to a formidable task in the short-term.

Argentina’s soaring Inflation and Interest rates under consecutive governments, Source: Reuter Graphics, Refinitiv Eikon, BCRA

Milei campaigned on two main policies, the first being massive cuts to public spending to slim down the Argentine state and the second, a divisive, ambitious plan to replace the Argentine Peso with the US Dollar.

Public spending in Argentina has been steadily climbing under successive Peronist governments rising from 26% of GDP in 2000 to 38% today which many on the right consider to be a key cause of inflation and inefficiency in Argentina, Milei intends to slash this figure by 15% of GDP to dramatically reduce the size of the Argentine state. Another polarising topic is public sector employment which has risen 34% between 2011 and 2022 helping fuel a 4% government budget deficit. The new President-elect is a strong advocate for the use of ‘shock therapy’ to correct the economy, planning to exchange the government deficit for a balanced budget in his first year by scrapping all electricity and gas subsidies, dissolving 10 of 18 government ministries and privatising all 34 of Argentina’s state run companies. Milei’s aspirations of increasing competition and efficiency in the Argentine economy extend to replacing infrastructure spending on public works with a private bidding system and scrapping privileged pensions for judges, diplomats and presidents. His economic vision of deregulation, reduction of state intervention and modernisation of the labour market to boost competitiveness is reminiscent of one of his political idols, Margaret Thatcher and Milton Friedman’s Monetarism after whom he named one of his five English Mastiffs.

Milei faces some clear barriers to his ambitious curtailment of public spending with investors showing clear concerns about the risks around governability given Argentina’s history of powerful labour movements and social protest. His government has not taken office as of time of writing, yet they already face enormous backlash over their plans to privatise the nations airline Aerolíneas from strong labour movements. Pablo Biró the leader of Argentina’s airline pilots union threatened that “if he wants to take Aerolíneas, he will have to kill us, and when I say kill, I mean literally: he will have to take dead bodies and I’ll sign up first.” highlighting that Milei will not easily revolutionise Argentina.

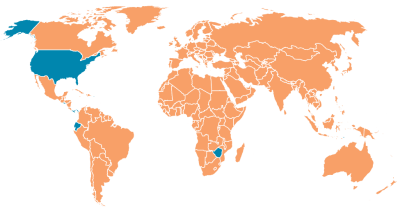

The most polarising policy for which Milei has captured world attention is the proposed dollarisation of the Argentine economy which involves intricate complexities both politically and economically to navigate. Argentina would not be the first Latin American country to pursue dollarisation with both El-Salvador and Ecuador being completely dollarised and Venezuela being pegged to the dollar with others around the world taking on a similar policy.

Countries that use the US Dollar in blue as of 2023, Source: Wise Voter

Advocates highlight that dollarisation could provide a credible stabilisation method which is naturally expansive by lowering the currency and counterparty risk. Dollarisation, they argue, would lower the interest rate risk through adopting a credible monetary regime, rallying government securities resulting in a capital gain. It could also result in an improvement in Argentina’s credit risk which historically has had a reputation of defaults, lowering interest rates resulting in an expansion improving fiscal numbers and reducing public spending. Milei also points out that the low demand for Argentina’s currency and high printing by the Central Bank makes Argentina a naturally inflationary economy. Argentina’s volatile political landscape could also no longer influence the currency if it was dollarised, a formula that Ecuador used to stabilise it’s economy. Emilio Ocampo, the leading voice in the proposition to dump the Argentine Peso for the US dollar argues that “the Argentine people have already chosen the dollar as their preferred currency”, with figures from the CATO institute supporting this: at the end of 2022, Argentines held over $246 billion in foreign bank accounts amounting to over 50% of Argentina’s GDP in current dollars. Argentines have been driven to hold the dollar to prevent savings being eroded by Argentina’s 143% inflation rate. Milei further rallied support for proposed dollarisation with his assertion that seigniorage has been a form of stealing from the regular Argentine by the political elite in Argentina to the degree of about 5% of GDP per year and dollarisation, he argues, would get rid of this.

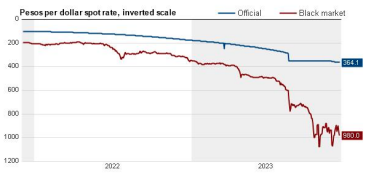

If dollarisation were to be pursued, it would likely take a similar form to that of the processes undertaken in Ecuador and El Salvador which dollarised in 2000 and 2001 respectively with a gradual estimated nine month transition from the peso-denominated monetary base to the equivalent in US dollars. Estimates suggest that Argentina’s dollar reserves would need to increase by $40 billion from the current $1.5 billion, Milei’s advisors have considered taxing dollar savings or using shares in the state owned oil firm as collateral for borrowing these dollars however both look ambitious given Milei’s weak position in Congress. It is very important that this is done at the correct monetary rate, dollarizing below the market rate would lead to a bank run as savers would attempt to protect their money from a forced devaluation and a rate over the market rate would see only to drive inflation further. Determining this rate has its own complexities and challenges with the black market rate of pesos to dollars varying drastically to the official rate. Last week the dollar was trading at about 1,020 pesos on the black market almost three times the officially fixed rate of 364 to the dollar. This caveat, while small, could still pose issues to the Argentine economy if this figure was miscalculated.

Argentina Pesos per US dollar: Official vs Black market, Source: Thomson Reuters Canada

For many economists, dollarisation doesn’t appear a realistic proposition. Those who do not support dollarisation look to the loss of monetary autonomy and inability to deal with country specific shocks using the Central Bank as a lender of last resort posing a risk for the Argentine economy. Furthermore, dollarisation would most likely require a very substantive loan to a country that has a long history of default. The IMF, who have given their largest loan ever to Argentina, have made their position clear that “dollarisation is not a substitute for sound macroeconomic policies” speaking to reporters in September. It is important for Argentina to remember that dollarisation will not solve all problems. The previous experiment in the 1990s of one dollar for one peso ended in 2001 with a bank crash, riots and a dramatic increase in the levels of poverty. While it stabilised prices in Ecuador, it did not stem the government’s fiscal deficits meaning that change within Argentine politics surrounding fiscal spending, which may not be popular with the electorate, must occur at the same time to fix Argentina’s economic woes if they were to dollarise. It should also be noted that dollarisation has only been adopted in small nations that rely on the flow of dollars from the sale of oil. Dollarisation can be used in oil rich nations to limit the extent of so-called Dutch Disease caused by relatively large oil exports driving up the price of local currency making other export sectors uncompetitive on the global market. Dollarisation in this case keeps currency stable to prevent fluctuations in local currency from changes in the global price of oil protecting other industries. Others suggest that default is the best way to fix Argentina citing that the country may be insolvent. Milei toned down his focus on dollarisation during the second round of presidential elections in order to win votes suggesting his government may attempt to take a more centre-right approach to the economy and in tackling Argentina’s problems. Adding to the uncertainty around dollarisation, Emilio Ocampo, the man Milei had said during the campaign would lead the Central Bank in closing it down, also turned down the role weakening Milei’s case for dollarisation further.

Milei’s impact on Argentina, while proposed to be revolutionary in reality, may struggle to make any real change given La Libertad Avanza’s weak influence in Senate and Congress. They hold less than 15 percent of seats in Argentina’s lower house, and in the Senate, it’s even weaker with Milei only having eight of the 72 seats. This means that Milei will have the weakest Congressional support of any president in Argentina’s history making the task of revolutionary change look even more unlikely. He will rely heavily on co-operation with former centre right president Macri who may offer his party’s support but on the issue of dollarisation, for which he would require a two-thirds majority vote, he would require the support of some Peronist’s which looks unlikely at least in the short term.

If his government can solve Argentina’s economic questions “it will be the best emerging market story in decades” according to the chief Latin America economist at Goldman Sachs, however if they get decisions wrong, the effects could serve to worsen Argentina’s woes. Whichever way it is framed, the Milei government has a daunting task when taking office on December 10th and some unpopular decisions to make. This is a delicate time for the Argentine economy with the most important question in the mind of all Argentines, how will the Milei government react?

References

1. Who is Javier Milei?, The Economist, 22/11/23

2. Can Javier Milei Save Argentina’s Economy? TLDR New Global 21/11/23

3. Argentina’s Milei on Dollarization, Central Bank, China Bloomberg television 19/08/23

4. Nugent, Luis Caputo takes on Argentina’s worst economic crisis in decades, Financial Times, 02/12/23

5. Nugent, Argentina’s Javier Milei names moderate ex-trader as economy minister, Financial Times, 29/11/23

6. Stott, Argentina’s Javier Milei backs away from dollarisation as central bank pick rejects role, Financial Times, 24/11/23

7. Stott and Nugent, How similar is Argentina’s Javier Milei to Donald Trump and Jair Bolsonaro?, Financial Times 26/11/23

8. Stott, The nightmare economic in-tray awaiting Argentina’s Javier Milei, Financial Times, 08/12/23

9. Stott, Argentina’s Milei faces enormous hurdles to govern, Financial Times, 20/11/23 10. Nugent, Argentina’s Javier Milei says he had ‘very comfortable’ meeting with Biden aides, Financial Times 28/11/23

11. Nugent, Argentina’s Javier Milei faces airline privatisation backlash, Financial Times 22/11/23

12. Ocampo, The case for dollarization in Argentina, 14/10/23